Preparing for your CPA appointment is one of the most important steps you can take to ensure a smooth and stress-free tax season. Whether you are managing personal finances or running a business in Litchfield Park, AZ, understanding what to bring to a CPA appointment can streamline the process and improve your tax outcomes. A thorough tax preparation checklist helps you gather all relevant documents, maximize deductions, and avoid filing delays or costly errors.

Many individuals and business owners in Arizona seek out qualified professionals for personal tax preparation and small business tax preparation. With proper planning and preparation, your CPA in Litchfield Park, Arizona, can help you navigate the complexities of tax regulations while optimizing your financial situation.

Understanding the Importance of Preparation

Walking into a tax meeting without the necessary paperwork can result in missed deductions, filing delays, or even penalties from the IRS. Preparation is more than simply collecting your W-2s and 1099s. It involves reviewing year-end tax documents, financial statements, deductions, credits, and even life events that could influence your filing status or tax liabilities.

Arizona tax preparation services, especially in growing communities like Litchfield Park, emphasize a proactive approach to income tax preparation. By knowing what to bring and organizing your records accordingly, you provide your CPA with everything needed to accurately file your returns and advise on future financial planning.

Whether you are a salaried employee, a self-employed professional, or a business owner, bringing the right information is the key to unlocking better tax results. CPAs are most effective when they have a complete view of your financial year, including income, expenses, and significant transactions.

Essential Documents for Individuals

For individuals seeking personal tax preparation in Arizona, having your income and deduction records ready is crucial. Begin with income documentation such as W-2 forms from employers and 1099 forms for freelance or contract work. Interest income from savings accounts or dividends from investments will typically be reported on 1099-INT and 1099-DIV forms.

Additionally, bring any documentation relating to unemployment income, Social Security benefits, or retirement distributions, which can impact your tax bracket and obligations. If you made any estimated tax payments throughout the year, provide receipts or confirmations to ensure they are correctly applied to your return.

Deductions and credits are another essential area. Medical expenses, charitable contributions, mortgage interest, and property taxes may qualify as itemized deductions. Records of tuition payments, student loan interest, or childcare costs can also unlock valuable tax credits. Health Savings Account (HSA) contributions and 529 education plan statements should be included as well.

Do not overlook personal changes that may influence your taxes. A marriage, divorce, birth of a child, or change in dependents will require documentation such as Social Security numbers and legal paperwork. These details help your CPA assess your eligibility for various tax benefits and ensure your filing status is up to date.

What Small Business Owners Should Bring

For small business tax preparation in Arizona, documentation goes beyond individual income. Business owners in Litchfield Park, AZ, should gather records that reflect the full scope of their operations. This includes gross receipts or sales reports, expense summaries, mileage logs, and payroll records if applicable.

Bring bank statements, credit card summaries, and invoices related to business expenses. These items help support deductions and validate business activity. Ensure you have documentation for any major purchases, asset depreciation schedules, and loan interest paid throughout the year.

If your business uses accounting software, export your profit and loss statement, balance sheet, and general ledger. These reports give your CPA an accurate overview of your business performance and can reveal opportunities for deductions or restructuring.

Also bring records of estimated tax payments and payroll tax filings. Business structure documents, such as your LLC operating agreement or articles of incorporation, may also be needed depending on the nature of your return. If your business operates in multiple states, provide relevant registration and tax documents for each jurisdiction.

Special Considerations for Arizona Taxpayers

Litchfield Park residents benefit from working with a CPA in Litchfield Park, Arizona, who understands the nuances of state and local tax laws. Arizona tax preparation services consider both federal and state regulations, and you will need to bring documents that apply specifically to your Arizona tax return.

Arizona offers unique credits and deductions, such as the Arizona charitable tax credit, which requires donation receipts from qualifying organizations. Contributions to Arizona 529 plans can provide additional state-level benefits. Discuss these opportunities with your CPA and bring supporting documentation if you’ve contributed.

Homeowners in Arizona may also be eligible for property tax relief programs or energy-efficient home improvement credits. If you installed solar panels, upgraded your HVAC system, or made other qualifying improvements, bring proof of purchase and any related manufacturer certifications.

Keep in mind that certain types of income may be taxed differently at the state level. Rental income, for instance, may require you to register with the Arizona Department of Revenue and file additional schedules. Your CPA can help you navigate these rules, but only if you provide all relevant details and documentation.

Creating a Personalized Income Tax Preparation Checklist

Using a customized income tax preparation checklist tailored to your situation can help ensure that nothing is overlooked. While your CPA may provide a general list, taking time to review your own financial records in advance will make your appointment more productive.

Start by gathering identification documents for yourself and all dependents. This includes Social Security cards and valid photo IDs. Then move on to income-related paperwork, such as W-2s, 1099s, K-1s for partnerships, rental income statements, and any relevant foreign income records.

Next, focus on deductions. Compile receipts and statements for deductible expenses, including education costs, charitable donations, retirement contributions, medical bills, and home office expenses if you are self-employed.

Review your year-end tax documents thoroughly. These often arrive by mail or electronically from banks, employers, and investment firms in January or February. Keeping a file or digital folder for tax documents throughout the year can reduce last-minute scrambling.

Organize your records in a logical order. Consider categorizing them into sections: income, deductions, credits, business records (if applicable), and previous tax returns. Bringing a copy of last year’s tax return can help your CPA identify carryover items and ensure continuity.

Conclusion

Being prepared for your CPA appointment is essential for a successful tax season. Whether you are focused on personal tax preparation in Arizona or managing small business taxes, coming equipped with the right documents will save time, reduce errors, and improve your results. Litchfield Park residents can benefit from the local expertise of a CPA in Litchfield Park, Arizona, who understands both federal and state-specific tax rules.

Use your income tax preparation checklist to gather all documents needed for tax filing. This includes everything from W-2s and 1099s to receipts, logs, and legal paperwork. For Arizona taxpayers, do not forget to include state-specific credits, deductions, and any changes in your personal life that could affect your filing status.

With thoughtful preparation and the right guidance, tax season can become an opportunity to optimize your finances rather than a source of stress. Partner with a CPA who offers comprehensive Arizona tax preparation services, and take control of your financial future with confidence.

Need an Accounting Firm in Litchfield Park, AZ?

Priscilla A. Chesler CPA PC is a full-service accounting firm that offers highly personalized solution for your business, nonprofit or organizations. Priscilla gets to know client businesses in depth, often onsite, to ensure she can offer guidance and services that fit the needs of the organization. Her expertise and knowledge of tax law and best accounting practices are always current. Contact her today to learn more about what she can do for you!

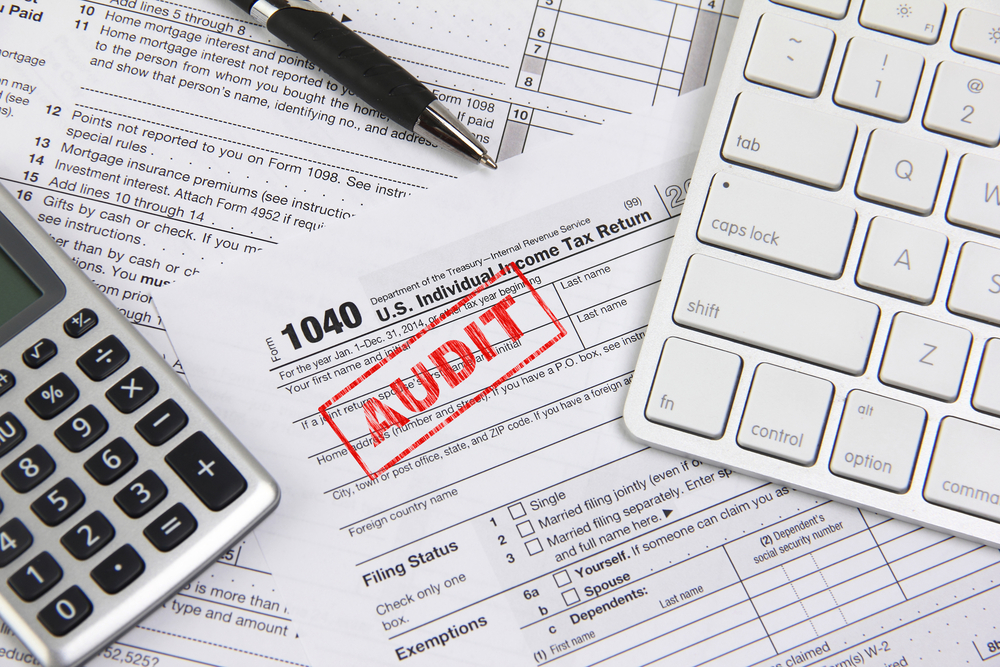

Tax season can be a stressful time for individuals and business owners alike. For residents and entrepreneurs in Litchfield Park, Arizona, the pressure to file an accurate tax return is heightened by the fear of being selected for an IRS audit. Understanding the most common IRS audit triggers and how to avoid them is essential to staying in compliance and maintaining peace of mind.

Whether you are managing your personal finances or running a small business, even honest mistakes can attract unwanted attention from the IRS. With the guidance of a knowledgeable CPA in Litchfield Park, Arizona, and a firm grasp on Arizona tax compliance, you can reduce your audit risk significantly and ensure your financial records remain in good standing.

High Income Levels and Large Deductions

While earning a high income is generally a positive achievement, it can also be one of the most well-known IRS audit triggers. Statistically, the IRS is more likely to examine returns from high-income earners, especially those with incomes exceeding $200,000 per year. If your earnings fall within this range, expect a higher level of scrutiny, particularly if your deductions appear disproportionate to your reported income.

Large itemized deductions, such as charitable contributions or medical expenses, can also raise red flags. If you are claiming deductions that are significantly higher than the average for your income bracket, the IRS may investigate to ensure they are legitimate. This does not mean you should avoid claiming deductions to which you are entitled, but rather that documentation and precise records are critical.

To protect yourself, maintain thorough documentation and ensure your deductions align with actual expenditures. Consulting with a CPA in Litchfield Park, Arizona, can help you assess whether your claims are reasonable and backed by appropriate evidence.

Reporting Business Losses and Cash Transactions

For small business owners, especially those in cash-intensive industries, reporting consecutive years of business losses is a significant audit trigger. The IRS may question whether your business is actually a for-profit endeavor or a hobby being used to offset other income. Small business tax audits often focus on whether expenses are ordinary and necessary for the business.

Additionally, cash transactions, whether in retail, food service, or other industries, tend to raise suspicion. The IRS is vigilant about underreported income, particularly when it comes to untraceable cash. Business owners who deal frequently in cash should take care to keep detailed logs and deposit records that reflect all income accurately.

If your business is reporting net losses year after year, it is essential to consult with a local CPA to evaluate your filings. A Litchfield Park, AZ, CPA can help ensure that your books are accurate, your expenses are legitimate, and your business operations are compliant with Arizona tax laws.

Inconsistent or Incomplete Information

Another one of the most common IRS audit mistakes is submitting a return that contains inconsistent or incomplete data. This includes discrepancies between your tax return and the forms submitted to the IRS by your employer, banks, or other third parties. For example, if the wages reported on your W-2 do not match your tax return, the IRS will likely notice the mismatch.

Mathematical errors, omitted forms, or incorrect Social Security numbers can also draw attention. While these may seem like minor oversights, they can delay processing or trigger an inquiry. The IRS uses automated systems to compare and cross-check data, and any irregularity may lead to additional scrutiny.

To avoid an IRS audit caused by such issues, double-check all information before filing. Electronic filing software can help reduce human error, but enlisting professional help from a CPA in Litchfield Park ensures that your return is prepared with the utmost accuracy. An expert eye can catch inconsistencies before they become problems.

Unusually High Charitable Donations or Home Office Deductions

Generosity is commendable, but when your charitable donations appear excessively high compared to your income, the IRS may raise an eyebrow. This is a common audit trigger for both individuals and business owners. The IRS may ask for substantiating evidence, such as donation receipts, written acknowledgments, and appraisals for donated items.

Similarly, home office deductions can lead to problems if not properly justified. Claiming part of your home as an office is a valid deduction if the space is used exclusively and regularly for business purposes. However, vague or exaggerated claims often attract attention, particularly when the deduction seems unusually large for the type of business being reported.

To protect yourself, ensure that your charitable contributions and home office expenses are well documented and fall within reasonable limits. Seek IRS audit help, Arizona-based tax professionals can walk you through the proper procedures for valuation and reporting, minimizing your audit risk while maximizing your legitimate deductions.

Failing to Report All Income or Foreign Accounts

Failing to report all sources of income is a major red flag for the IRS. This includes freelance income, investment earnings, rental income, and earnings from gig economy platforms. Even if you do not receive a 1099 form, you are still legally obligated to report all income. Many taxpayers mistakenly believe that small amounts or payments in cash are not taxable, which is incorrect and could lead to serious consequences.

Foreign accounts, trusts, and financial assets held overseas also fall under close IRS scrutiny. Taxpayers must report foreign bank accounts and other offshore assets if they exceed certain thresholds, using forms like the FBAR and FATCA disclosures. Neglecting to report such accounts can result in steep penalties.

For individuals and businesses alike, working with a Litchfield Park, AZ, CPA can make the difference between accurate reporting and costly mistakes. These professionals understand the nuances of tax return accuracy and can help you disclose income and assets correctly, whether domestic or international.

Conclusion

An IRS audit can be a daunting experience, but understanding the typical triggers can help you stay ahead of potential issues. From high incomes and disproportionate deductions to inconsistent data and underreported income, the IRS uses a range of indicators to select returns for closer examination.

With the support of a qualified CPA in Litchfield Park, Arizona, you can implement effective audit prevention strategies tailored to your financial situation. Maintaining thorough records, staying compliant with Arizona tax regulations, and reviewing your return carefully before submission are all critical steps in avoiding an audit.

If you are concerned about IRS audit triggers or need help with your taxes, seek guidance from a trusted Arizona tax compliance expert. Professional assistance not only enhances tax return accuracy but also provides peace of mind that you are doing everything right. Whether you are an individual taxpayer or a small business owner, smart planning and professional advice are your strongest tools in the fight against audits.

Need an Accounting Firm in Litchfield Park, AZ?

Priscilla A. Chesler CPA PC is a full-service accounting firm that offers highly personalized solution for your business, nonprofit or organizations. Priscilla gets to know client businesses in depth, often onsite, to ensure she can offer guidance and services that fit the needs of the organization. Her expertise and knowledge of tax law and best accounting practices are always current. Contact her today to learn more about what she can do for you!

Life’s major milestones are often filled with emotional and personal transitions, but they also come with significant tax implications that are too important to ignore. Whether you’re getting married, going through a divorce, or planning for retirement, each stage brings about new responsibilities and opportunities related to your taxes. Working with a local CPA in Litchfield Park can help you understand and navigate these shifts efficiently, avoiding penalties and taking advantage of potential tax-saving strategies.

Understanding how these life events affect your finances, especially in the context of Arizona income tax planning, can make all the difference in staying compliant with state and federal laws. Let’s explore how these common life changes can impact your tax planning and what steps you can take to stay ahead.

Marriage and Tax Implications

Getting married changes more than just your last name or your address. From a tax standpoint, it alters how you file, how much you pay, and what deductions or credits you may qualify for. The first decision you’ll need to make is whether to file jointly or separately. In most cases, filing jointly offers more favorable tax rates and greater access to credits, such as the Earned Income Tax Credit or education-related benefits. However, there are situations where filing separately may be advantageous, such as when one spouse has significant medical expenses or miscellaneous deductions.

Marriage tax implications are especially important to consider during the first year after your wedding. If you and your spouse are both earning income, you may move into a higher tax bracket combined, which is commonly referred to as the “marriage penalty.” On the flip side, if one spouse earns significantly less than the other, marriage can actually lower your total tax bill.

Updating your W-4 form with your employer is another crucial step. Your new marital status could change your withholding amount, which can prevent you from owing a large tax bill when filing next April. In Arizona, where state income tax applies, coordinating your withholding with the guidance of a CPA in Litchfield Park, AZ ensures both spouses are correctly prepared at the state and federal levels.

Divorce and Tax Considerations

Divorce is a difficult life event that carries emotional, legal, and financial challenges. Amid the legal paperwork and division of assets, taxes can often become an overlooked consequence. Yet divorce tax considerations can significantly impact both parties’ financial outcomes for years to come.

One of the most important changes is your filing status. You may need to switch from married filing jointly to either single or head of household. Filing as head of household often provides more favorable tax brackets and larger standard deductions, but specific requirements must be met, including having a dependent and paying more than half the cost of maintaining a home.

Another factor is alimony. Under federal law, for divorces finalized after 2018, alimony payments are no longer deductible for the payer, nor are they considered taxable income for the recipient. This change significantly shifts the tax burden compared to earlier rules, and many Arizona residents are unaware of this adjustment. Partnering with a professional who understands tax planning for life changes can help mitigate any negative impact.

Custody and dependent claims also influence who gets to benefit from child-related tax credits. Only one parent may claim the child tax credit, education credits, and dependent care credits. Misunderstanding these rules can result in IRS penalties and delayed refunds. A local CPA in Litchfield Park can help newly divorced individuals or co-parents structure agreements that comply with state and federal tax regulations while maximizing tax savings.

Retirement and Tax Planning in Arizona

Retirement is often seen as a time to enjoy the rewards of a life well worked, but it also presents new challenges related to income, budgeting, and taxes. Withdrawing money from retirement accounts, starting Social Security benefits, and managing other income sources all have tax consequences. This is where strategic retirement tax planning in Arizona becomes crucial.

Arizona offers several tax benefits to retirees. Social Security income is not taxed by the state, and public pension income from sources like the military or certain government jobs may also be partially exempt. However, other retirement income, such as 401(k) or IRA distributions, is subject to Arizona state income tax. This makes it essential to plan withdrawals carefully to avoid pushing yourself into a higher tax bracket.

Required Minimum Distributions (RMDs) also begin at age 73, and failing to take these mandatory withdrawals can result in steep IRS penalties. Tax planning professionals can help spread out your income in retirement to minimize the tax impact year over year.

In addition, tax help for retirees in Arizona is critical when managing Medicare surcharges. If your adjusted gross income exceeds certain thresholds, you may face higher Medicare premiums. Proper tax strategies, including Roth conversions or timing of income, can help manage this effectively.

Planning for Life Changes with a Local CPA

All these major life events, marriage, divorce, and retirement, highlight the importance of proactive, customized Arizona tax planning. These transitions affect not just your current tax situation but also your long-term financial outlook. Whether you’re merging finances with a spouse or redefining your retirement budget, having a knowledgeable advisor by your side makes a substantial difference.

A local CPA in Litchfield Park who understands both state-specific laws and federal tax codes can offer tailored advice for each stage of your life. They can review your financial documents, assist with income tax filings, and provide strategies that optimize your deductions and credits. They can also ensure that business income, rental property, and investment accounts are properly reported and structured to minimize liability.

For small business owners, this type of guidance becomes even more critical. Combining small business and personal tax planning helps entrepreneurs navigate personal milestones while still keeping their business interests in focus. For example, a divorce could affect ownership stakes, while retirement might mean planning an exit strategy with tax consequences.

Navigating Arizona Income Tax Planning Year-Round

Effective Arizona income tax planning doesn’t happen once a year during tax season. Instead, it should be an ongoing process that adapts as your life evolves. Whether you’re buying a new home, expanding your family, or considering early retirement, each decision can create ripple effects in your tax profile.

The key to minimizing surprises and maximizing savings is regular check-ins with a trusted tax advisor. They can help you project future tax liabilities, recommend timely tax-saving moves, and ensure you’re making the most of Arizona’s tax benefits. Whether it’s adjusting your withholdings after a marriage or optimizing IRA distributions in retirement, these steps help you avoid costly mistakes.

Conclusion

Life’s big changes often come with a mix of excitement and uncertainty, but one thing is clear: they all carry tax consequences that can impact your financial health. Whether you’re navigating marriage tax implications, addressing divorce tax considerations, or crafting a smart retirement tax planning in Arizona strategy, proper guidance is essential.

Partnering with a CPA in Litchfield Park, AZ ensures you’re not just reacting to tax changes but preparing for them in advance. This proactive approach protects your income, reduces your tax liability, and provides peace of mind during life’s most pivotal transitions. With expert tax planning for life changes, you can move forward confidently knowing that your financial future is built on a solid and tax-efficient foundation.

Need an Accounting Firm in Litchfield Park, AZ?

Priscilla A. Chesler CPA PC is a full-service accounting firm that offers highly personalized solution for your business, nonprofit or organizations. Priscilla gets to know client businesses in depth, often onsite, to ensure she can offer guidance and services that fit the needs of the organization. Her expertise and knowledge of tax law and best accounting practices are always current. Contact her today to learn more about what she can do for you!

As the end of the calendar year approaches, Arizona business owners must turn their attention to one of the most critical aspects of business operations: taxes. Preparing for tax season isn’t just about filing paperwork. It’s an opportunity to assess your financial position, take advantage of deductions, and plan strategically to minimize your tax burden. Whether you’re a seasoned entrepreneur in Phoenix or a growing small business in Litchfield Park, CPA for businesses can provide valuable guidance. However, understanding what to do before December 31st is key to efficient business tax planning in Arizona.

In this comprehensive guide, we’ll walk through a detailed business tax checklist for Arizona businesses. With the right year-end tax tips for Arizona businesses, you can approach tax season with confidence and possibly improve your bottom line.

Review Financial Statements and Reconcile Accounts

The foundation of smart year-end business tax planning in Arizona begins with a thorough review of your financial records. Business owners should ensure their income statements, balance sheets, and cash flow statements accurately reflect the year’s transactions. Reconciling all bank accounts, credit cards, and loan balances is critical to verify that all financial activity has been properly recorded.

Errors or inconsistencies in your books can lead to inaccurate tax filings, missed deductions, or even red flags for audits. For those in cities like Scottsdale, Mesa, or Litchfield Park, CPA for businesses can provide a trained eye to catch discrepancies that might otherwise go unnoticed. They can also guide you on categorizing expenses correctly, an essential step for claiming all legitimate deductions available under Arizona tax regulations.

Reviewing financials also helps businesses assess their profitability, debt load, and cash reserves. These insights are crucial not just for tax filing, but also for long-term planning and growth strategies. As a bonus, having clear records positions your business favorably in case you seek financing or investors in the new year.

Maximize Deductions and Depreciation Strategies

One of the most beneficial aspects of the business tax checklist for Arizona businesses is identifying all available deductions. From vehicle expenses and business meals to rent, utilities, and employee benefits, these deductions reduce your taxable income and can make a substantial difference in your final tax bill.

Arizona businesses should also evaluate depreciation opportunities for equipment and capital expenditures. The Section 179 deduction and bonus depreciation provisions allow companies to write off the entire cost of qualifying equipment in the year it was placed into service, rather than depreciating it over several years. If your business made major purchases in 2025, ensure those assets are in use before December 31 to take full advantage of this provision.

It’s worth noting that tax codes change frequently. That’s why many small businesses rely on professionals in tax-focused towns like Litchfield Park. CPA for businesses can provide personalized year-end tax tips for Arizona businesses to ensure you don’t overlook valuable tax-saving opportunities. Working with a CPA can also help you balance current-year tax savings with long-term depreciation strategies, which can be critical for multi-year planning.

Review Payroll and Employee Benefits

Payroll compliance is an often-overlooked but essential part of Arizona business tax planning. Before the year ends, verify that all payroll records are up to date, including wages, bonuses, and employee benefits. Businesses must ensure they’ve correctly withheld federal and Arizona state taxes, Social Security, and Medicare contributions.

If your business offers fringe benefits, such as health insurance, retirement plans, or stock options, now is the time to make sure these are accurately reflected in your accounting and W-2 forms. Proper documentation not only satisfies IRS requirements but also supports claims for deductions or credits, such as the Work Opportunity Tax Credit or Arizona-specific employment incentives.

If you’re planning to issue year-end bonuses, make sure those payments are processed before December 31 to be included in this year’s tax filings. Depending on your financial outlook, you may also want to prepay some 2026 wages or benefits to shift deductions into the current year.

An experienced CPA for businesses in Arizona can advise whether accelerating or delaying payroll expenses makes sense for your specific financial situation. These decisions should be based on projected revenue, expected tax rates, and the overall health of your business.

Plan for Estimated Taxes and Review Tax Elections

Another critical step in the business tax checklist for Arizona businesses is reviewing your estimated tax payments. Most Arizona businesses, especially sole proprietors, S-corporations, and LLCs, must make quarterly estimated tax payments. Missing these or underpaying can lead to penalties and interest. As the final quarter closes, review your payments to determine if a top-up is necessary before year-end.

Business owners should also take the time to revisit their entity structure and tax elections. For example, some LLCs may benefit from electing to be taxed as an S-corporation to take advantage of reduced self-employment taxes. These decisions can have significant implications on your tax liability and should be evaluated before the start of a new tax year.

Companies that operate across state lines should also verify whether they owe any Arizona transaction privilege tax (TPT) or use tax. Ensuring compliance with Arizona-specific business tax obligations can help avoid costly audits or fines.

If you haven’t already, consider sitting down with a local Arizona tax professional. Someone familiar with business tax planning in Arizona can ensure you’re not missing key elections, credits, or strategies that could help you now and in the years to come.

Evaluate Retirement Contributions and Charitable Giving

Many tax-saving strategies are tied to retirement planning and charitable giving, two areas that can be particularly beneficial for both businesses and business owners as individuals. If your business sponsors a 401(k) or SEP IRA, make sure all employer contributions are processed before year-end to qualify for a 2025 deduction. If you don’t yet offer retirement options, now is an ideal time to set up a plan, even if it won’t take effect until 2026.

For business owners looking to reduce taxable income, charitable contributions are another useful tool. Arizona offers tax credits for donations to qualifying charitable organizations, school tuition organizations, and foster care charities. These credits can be used in addition to federal deductions, providing dual tax benefits.

However, these contributions must be made by December 31 to be counted toward the current tax year. Be sure to retain all receipts and documentation, especially for non-cash donations. If your business is structured as a pass-through entity, these deductions may impact your personal tax return as well.

Working with a knowledgeable CPA for businesses ensures that you optimize these contributions not only for tax purposes but also to align with your business’s community values and long-term financial goals.

Conclusion

The final weeks of the year are a crucial time for Arizona business owners to get their tax affairs in order. With a clear business tax checklist and proactive business tax planning in Arizona, you can significantly reduce your tax burden, avoid penalties, and enter the new year with financial clarity. From reconciling your books to maximizing deductions and reviewing your tax elections, each action you take now sets the tone for your future success.

Whether you’re managing a large operation or running a small business in Litchfield Park, CPA for businesses can provide customized support to help you make informed decisions. These year-end tax tips for Arizona businesses are not only about compliance but about building a stronger, more resilient business.

Before December 31 arrives, invest the time and resources needed to wrap up your year the right way. Smart planning today can yield meaningful tax savings tomorrow, making it one of the most rewarding investments you can make as a business owner in Arizona.

Need an Accounting Firm in Litchfield Park, AZ?

Priscilla A. Chesler CPA PC is a full-service accounting firm that offers highly personalized solution for your business, nonprofit or organizations. Priscilla gets to know client businesses in depth, often onsite, to ensure she can offer guidance and services that fit the needs of the organization. Her expertise and knowledge of tax law and best accounting practices are always current. Contact her today to learn more about what she can do for you!

Tax season can be a stressful time for many families, especially when it feels like you’re leaving money on the table without realizing it. For Arizona residents, knowing how to make the most of your tax situation is key to keeping more of your hard-earned income. While most people remember to claim the standard deductions and some itemized ones, there are several overlooked tax breaks for families that could make a significant difference in your refund or tax liability. If you live in Arizona and want to make sure you’re not missing out, it might be time to reconsider your approach, especially with the help of a qualified tax professional like a CPA in Litchfield Park.

The Importance of Strategic Tax Planning for Arizona Families

For families living in Arizona, tax planning isn’t just a once-a-year task—it should be an ongoing strategy. Many taxpayers wait until April to think about deductions, but proactive planning can reveal opportunities that are otherwise missed. Taxpayers with children, home offices, or education expenses often qualify for additional deductions and credits, but fail to claim them simply because they’re unaware.

Arizona offers several unique tax credits and deduction opportunities tailored to families. For example, the state provides tax credits for private school tuition, public school extracurricular fees, and contributions to qualifying charitable organizations. These can directly reduce your state tax liability and often go unused.

A common oversight among Arizona families is failing to adjust withholdings or contributions to benefit from tax-saving opportunities throughout the year. When you consult a CPA, you can assess your financial situation holistically, identify potential tax breaks, and make real-time adjustments that put your family in a stronger position when tax season arrives.

Hidden Family Tax Breaks That Often Go Unclaimed

Despite a variety of family-related tax benefits, many households miss valuable deductions due to lack of awareness or incorrect filing. Among the most commonly overlooked tax breaks for families is the Child and Dependent Care Credit. This credit can offset the cost of childcare for children under 13 or for a dependent who is physically or mentally unable to care for themselves. If you pay a daycare, after-school program, or even a babysitter so you can work or look for work, you may qualify.

Education expenses are another frequently neglected deduction. The American Opportunity Credit and the Lifetime Learning Credit can offer thousands in savings for families paying for college or other post-secondary education. Even if you or your child didn’t attend school full-time, partial enrollment often still qualifies.

Homeownership also opens up doors for deductions. Mortgage interest, property taxes, and even certain energy-efficient home improvements can be claimed. Arizona families upgrading their homes with solar panels or energy-efficient appliances may be eligible for state and federal tax credits. A reliable tax preparer near Litchfield Park can walk you through the specifics to ensure you capture all that you’re entitled to claim.

The Value of Localized Knowledge From a Tax Preparer Near Litchfield Park

When it comes to maximizing deductions and uncovering hidden opportunities, working with a tax preparer near Litchfield Park can be a game changer. National tax software programs and large chains may not understand the nuances of Arizona-specific tax laws, let alone the subtleties of the local economy or recent updates in the state’s tax code.

A CPA is more likely to be familiar with regional credits such as the Arizona School Tax Credit or the state’s provisions for foster care charitable organizations. These deductions often go overlooked by families who rely solely on generic tax tools.

Additionally, if your family owns a small business or works in a freelance capacity, a local tax professional can assist with finding deductions that apply to your unique situation. These might include business use of your home, vehicle expenses, health insurance premiums, and retirement contributions. Understanding where personal and business finances intersect is critical in maximizing deductions, and a knowledgeable CPA near Litchfield Park is well-equipped to provide this guidance.

Arizona Family Tax Tips That Go Beyond the Obvious

While many families in Arizona are familiar with basic deductions, the real advantage lies in digging deeper. For example, families who adopt children can qualify for an adoption tax credit, which helps offset legal and administrative costs. Arizona also offers additional support to adoptive parents at the state level, a fact not commonly known without professional insight.

Another helpful but underutilized strategy involves Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). Contributions to these accounts are pre-tax and can be used for medical expenses, reducing your taxable income. Many Arizona families dealing with medical costs miss out on these benefits because they don’t plan early enough in the year to take advantage.

Arizona also allows for a tax credit when donating to Qualified Charitable Organizations (QCOs) and Qualified Foster Care Charitable Organizations (QFCOs). These credits can directly reduce the amount of taxes owed dollar-for-dollar, unlike deductions which only reduce taxable income. Making such donations before the tax deadline is a smart way for Arizona families to support the community and boost their own financial standing.

How to Make Sure You’re Not Missing Out

It can be challenging to keep track of every deduction and credit available, especially when tax laws change from year to year. That’s why so many Arizona families benefit from working with a local professional who specializes in state-specific tax preparation. If you’re wondering whether you’ve taken advantage of all possible savings, now is the time to reach out to a tax preparer near Litchfield Park who can provide personalized support.

The first step is organizing your documents. Keep receipts for school fees, medical costs, charitable donations, and childcare expenses throughout the year. Then, when it’s time to file, your tax preparer can determine which of these qualify under current Arizona law. Also, make a habit of reviewing your financial goals annually with your CPA to ensure you’re aligned with the most up-to-date Arizona family tax tips and strategies.

Additionally, consider conducting a mid-year tax check-in. This allows you to assess how you’re doing compared to projections, whether you should adjust your withholdings, and if there are opportunities for additional deductions before the year ends.

Conclusion

For Arizona families, maximizing tax deductions requires more than just filing on time. It takes a proactive, educated approach, combined with the help of a knowledgeable tax preparer near Litchfield Park. From overlooked tax breaks for families to Arizona-specific credits and deductions, there are many ways to reduce your tax liability and keep more money in your household budget.

A local CPA brings a level of personal insight and familiarity with Arizona’s tax code that national services simply can’t match. Whether it’s taking advantage of the Arizona School Tax Credit, claiming all available childcare credits, or optimizing your HSA contributions, small strategies add up to big savings. With the right planning and guidance, Arizona families can make tax season a time of opportunity rather than stress.

If you’re unsure whether you’ve claimed everything you’re entitled to, now is the perfect time to consult a CPA. Your future self—and your wallet—will thank you.

Need an Accounting Firm in Litchfield Park, AZ?

Priscilla A. Chesler CPA PC is a full-service accounting firm that offers highly personalized solution for your business, nonprofit or organizations. Priscilla gets to know client businesses in depth, often onsite, to ensure she can offer guidance and services that fit the needs of the organization. Her expertise and knowledge of tax law and best accounting practices are always current. Contact her today to learn more about what she can do for you!